Most buyers think the homes around them are selling to families like theirs — financed, FHA or conventional, scraping together a down payment and going up against a couple other offers.

That’s not what the April 2026 numbers say.

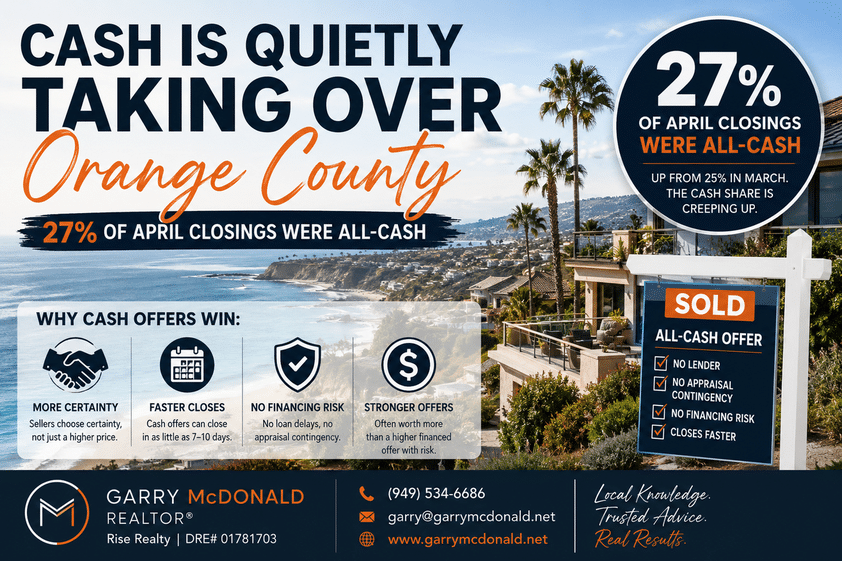

More than 1 in 4 closed sales in Orange County last month — 27% — were all-cash. In March it was 25%. The cash share is creeping up, not down, even as inventory has loosened.

If you’re buying with a loan in this market, that single number changes how you should write offers, what you should expect from sellers, and where you can actually compete.

What “27% cash” really means

When the report says 27%, it doesn’t mean 27% of buyers happen to have a checking account big enough to pay cash. It means 27% of closed transactions had no lender, no appraisal contingency, no underwriting timeline, and no financing risk.

For a seller looking at three offers, that’s not just a different price — it’s a different kind of certainty. A clean cash offer that closes in 10 days is often worth $20,000–$30,000 less than a financed offer that needs 30 days, an appraisal, and a loan contingency.

That’s the math sellers are doing in their head. And in April, more than a quarter of them said yes to it.

Where the cash is coming from

Three groups are driving most of it in Orange County:

- Move-up sellers who sold a home elsewhere — sometimes out of state — and are rolling the proceeds into a smaller, often coastal property

- Trust and inheritance buyers purchasing in their family’s name with liquidated assets

- Investors and second-home buyers who don’t want to deal with rate volatility and just want the asset

The first group is the most relevant for everyday buyers, because they’re competing for the same houses you are — and they’re not going away.

What this means if you’re buying with a loan (73% of you)

The good news: 73% of April’s closings were still financed. You are not locked out of this market. You are just operating in it.

A few things that actually move the needle against cash:

- Get fully underwritten before you write offers. Not just pre-approved — underwritten. The seller’s agent can call your loan officer and confirm the loan is essentially “cash-equivalent.”

- Shorten your contingencies. A 17-day inspection / 21-day loan timeline can be tightened to 7 / 14 with the right team. Sellers feel that.

- Be willing to release earnest money sooner. It signals you’re serious, not just shopping.

- Don’t waive the appraisal blindly. Cash buyers don’t need one. You do — but you can structure an “appraisal gap” clause that covers a defined dollar amount instead.

None of these things require you to be a cash buyer. They just require you to be the least risky financed offer in the stack.

What this means if you’re selling

If you’re listing in the next 60 days, you’re going to see cash offers. Some will be real. Some will be lowballs from investors testing the water.

Two things to evaluate, in order:

- Proof of funds dated within the last 30 days, from a major institution. “Cash” from a portfolio that needs to be liquidated is not the same as cash already sitting in a checking account.

- Net to you after closing costs and credits. A financed offer at $1,425,000 with reasonable terms may net you more than a cash offer at $1,395,000 with no contingencies but a 7-day close that forces you into a rental.

The goal isn’t to take cash. The goal is to take certainty at the right price.

The bottom line

The cash share in Orange County keeps inching up, and there’s no signal that’s about to reverse. That doesn’t mean the market is broken for the 73% buying with a loan — it means the standard playbook from 2020 doesn’t work anymore. You compete on terms, timeline, and clean structure, not just price.

If you’re trying to figure out where you actually stand in this market — as a buyer or a seller — I’d rather walk you through it on a 15-minute call than have you guess. Reach out anytime.

Garry McDonald | REALTOR®

Rise Realty | DRE# 01781703

📞 (949) 534-6686

✉️ garry@garrymcdonald.net

🌐 www.garrymcdonald.net