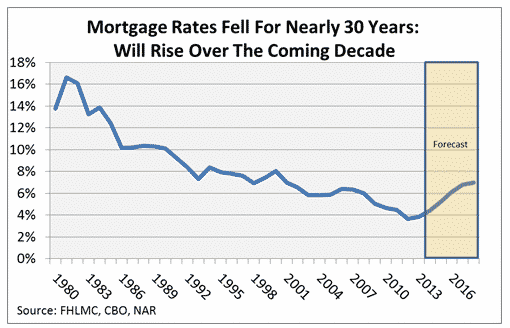

Rates for the 30-year FRM fell steadily over the last 30 years, but that trend is likely now at an end. Economic growth and the imminent end of the Fed’s MBS and Treasury purchase programs will likely cause long-term borrowing rates to rise over the next decade. This trend will present both lenders and consumers with challenges. Lenders will need to balance the risks of rising interest rates on deposits against fixed returns on portfolios of long-term mortgages. Likewise, mortgage backed securities with low coupons, or the rate paid to investors who own them, will fall in value as mortgage rates rise, creating headwinds for that funding channel. Consumers on the other hand will need to modify expectations for affordability and purchasing power as rising rates and inflation will erode both unless income growth can rise enough to compensate.